Latest News

NextGen Broadcasting Takes on TikTok With Interactive Fast Stream Technology

Pearl group stations join Sinclair in launching local and national channels

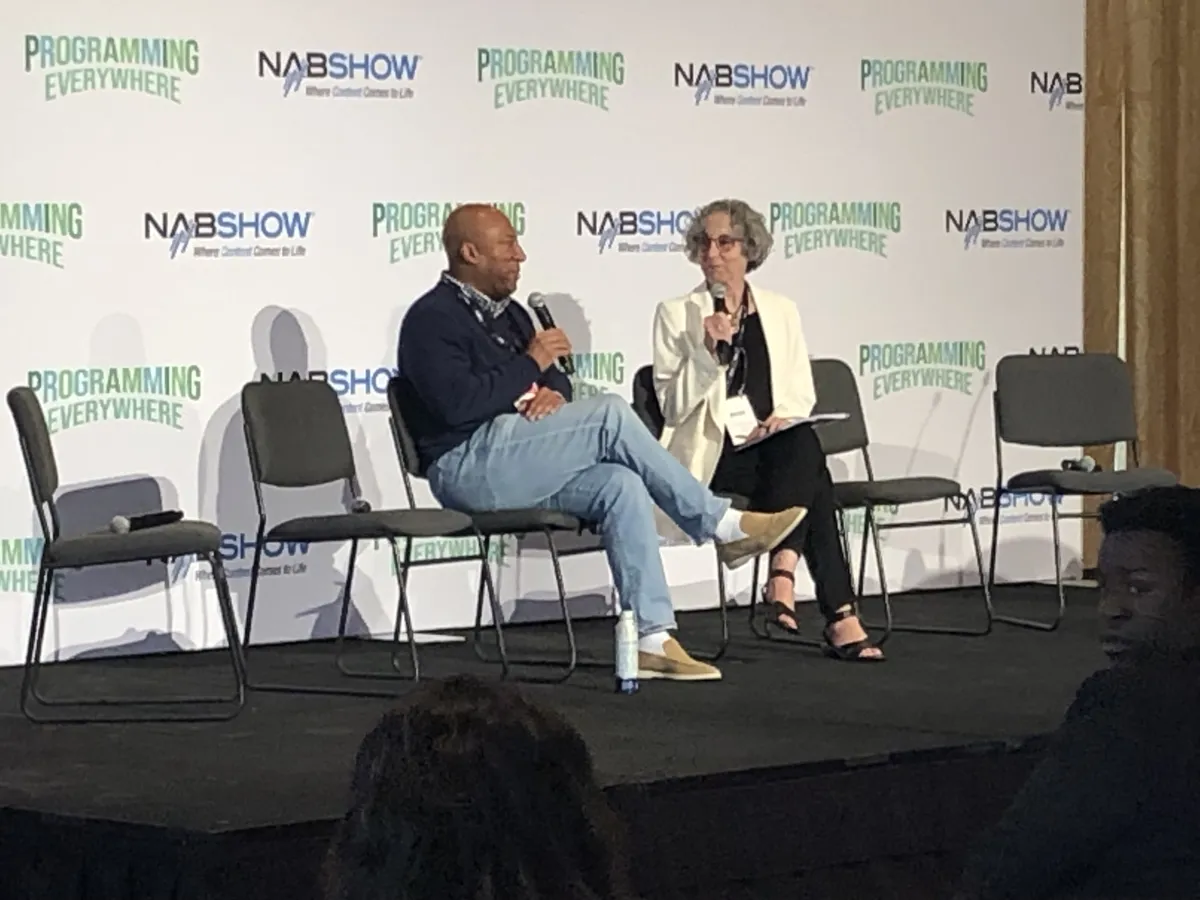

Byron Allen Says What He’d Do With Paramount Global (NAB Show)

Lays out key points for local broadcasters to stick around long-term

Sinclair Launches Broadspan Datacasting Platform

Datacasting expected to relieve traffic as video clogs the internet

‘Star Trek: Strange New Worlds’ Gets Season 4 on Paramount Plus

Fifth season of ‘Star Trek: Lower Decks’ will be final one

Dog Whisperer Plays ‘Matchmaker’ in New Season of ‘Better Human Better Dog’

Cesar Millan lights up Empire State Building before season starts on Nat Geo

‘The Talk’ Will Return to CBS for Shortened 15th Season

Daytime talker will conclude in December

Mary Connelly, Executive Producer of ‘Jennifer Hudson,’ To Exit

Mary Connelly previously executive-produced ‘Ellen DeGeneres’

Broadcasters Invest in Run3TV To Bolster Over–the-Air Audience Measurement

Nielsen, Comscore explore ways to use data from NextGen sets

MOST READ